The excitement about changing career paths is incomparable! You pursue your long-awaited dream, want to restore the right work-life balance, or simply try something totally new. Although, despite all the joys and professional rewards, your finances should also be carefully taken care of in case you decide to change jobs. After all, any career change entails a change in monthly payments, which, in its turn, influences your ability to cover necessary expenses.

Assessment of how your finances will be affected by the planned career change is a prerequisite for making the process seamless and hassle-free. To be able to focus on the job duties of your new position fully, you need to think carefully about your financial situation in advance and develop certain strategies.

How to Assess Your Financial Situation Prior to a Career Change

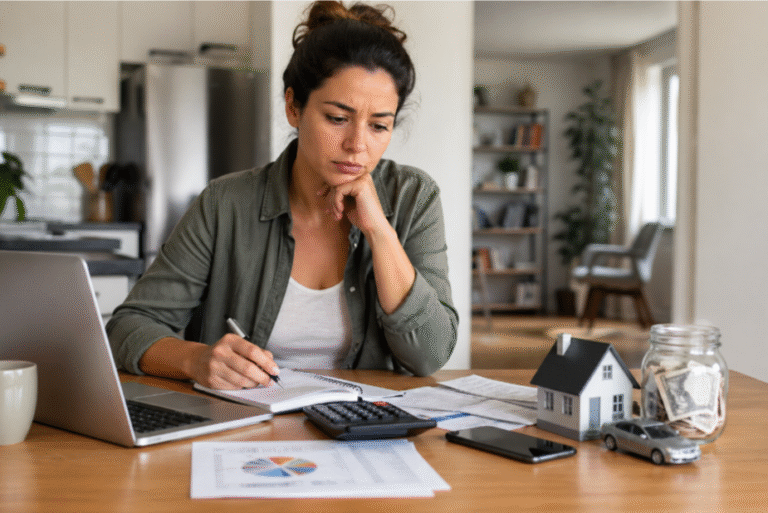

The most appropriate approach to beginning the process of transitioning to a different occupation is a thorough assessment of your current financial situation. The primary task here is to learn more about your current income, your fixed expenditures, and your variable expenses. Therefore, open your banking app and assess your transactions during the last three-six months.

To begin with, note the figures related to your fixed expenses, including the cost of accommodation, mortgage repayments, insurances, and utilities payments. Also, determine the sum that you spend every month on groceries, entertainment, and meals out. Understanding what your living expenses are equal to will enable you to identify the minimum amount that you must earn in order not to become financially vulnerable after the career change.

Creating the Transition Budget

After analysing your expenditure, you can proceed to developing your budget for the period of transition to a different occupation. In most cases, when switching careers, you have to either get a new degree, start from scratch in a new field, or move jobs, which results in reduced salary. Hence, you must plan your expenditure considering this circumstance.

First, think of the things you can live without. Cancel your streaming subscriptions, visit fewer restaurants, and try to entertain yourself free of charge. This approach will help you minimise your expenditure in the shortest possible time.

Managing Debt and Savings

Finally, it is critical to handle your current debts and properly use your savings to avoid unnecessary financial difficulties during the period of transition.

As a rule, any drop in income negatively influences one’s ability to cover their loan liabilities, especially mortgage repayments. As soon as you have realised that you want to change your job and will likely see some fluctuations in your income, contact the representatives of the bank. There are a lot of ways of solving such issues, including temporary postponement of payments and refinancing to a more favourable interest rate. Companies like have many products and resources to explore.

An emergency fund was created precisely for the times like these. Thus, if you have money saved, calculate how many months you will be able to cover your expenses using this money. Also, try to distribute your savings in such a way that the amount you receive in your current account per week would imitate your salary and would help you maintain the newly developed budget.